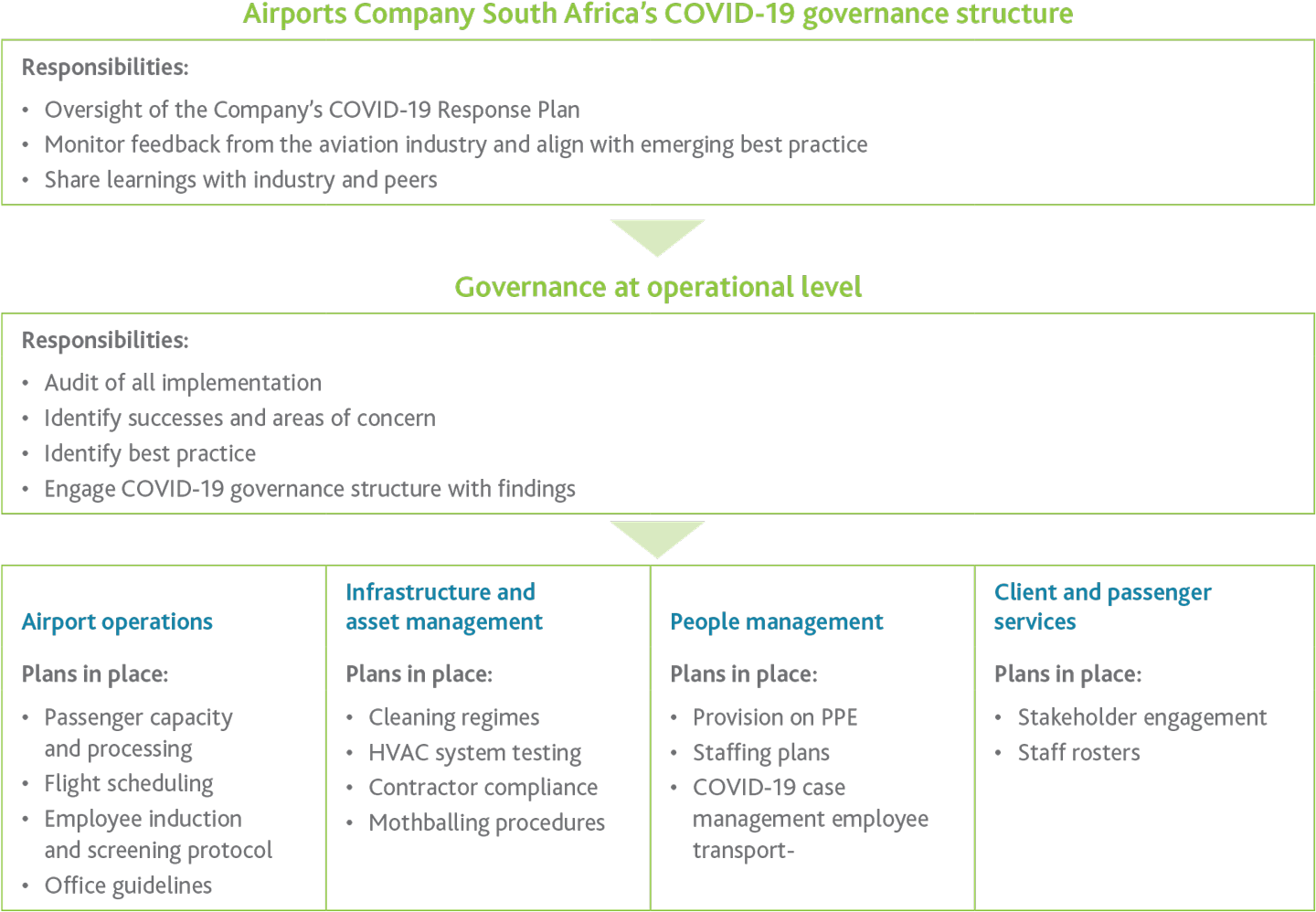

Our COVID-19 response programme, which was still in place throughout the reporting period, is illustrated in the following graphic:

At our other airports, local occupational health service providers are contracted through a nationally appointed service provider to deliver consistent service to all staff and airport users.

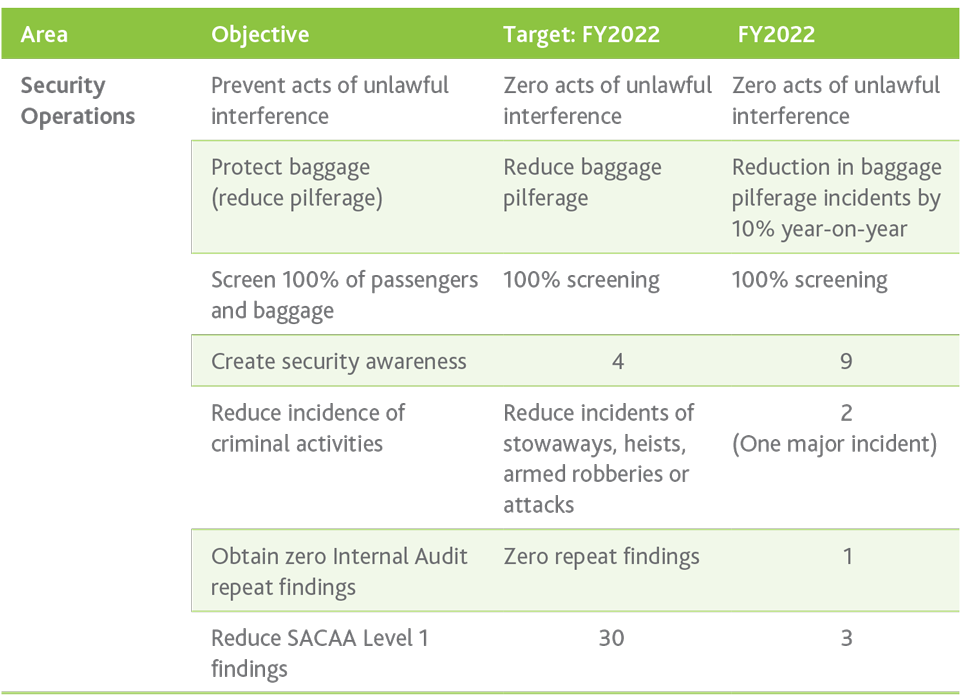

A key focus of enterprise security during the various levels of lockdown was the protection of our perimeters and access gates as well as the prevention of vandalism of infrastructure. We heightened security measures by increasing law enforcement visibility in and around our airports and reduced access to the airside and terminal buildings.

OUTLOOK

With COVID-19 restrictions having been lifted post year-end on 22 June 2022, we are able to begin the long journey towards recovery and development in earnest.

During the current period and going forward, we will remain focused on our core business of running airports and will continue to strive for continuous improvement in the passenger experience. Simultaneously, we will focus on extending and developing our cargo handling capabilities and the services we offer to our customers in the cargo and logistics businesses.

More ambitiously, we are aiming to redefine the place of the airport in city life and to make airport hubs more attractive leisure destinations for both passengers and the public in general. We intend to do this by diversifying our range of services and by working towards creating an integrated and interconnected aerotropolis at each of our airports. We will continue to do so in cooperation with our shareholder, our business partners and all of our stakeholders.