While COVID-19 continued to impact on our operations throughout the reporting period, we have reconfigured our organisation in such a way that it is more flexible than it was before the pandemic and more readily adaptable to change, even at short notice.

PERFORMANCE REPORT

OVERVIEW

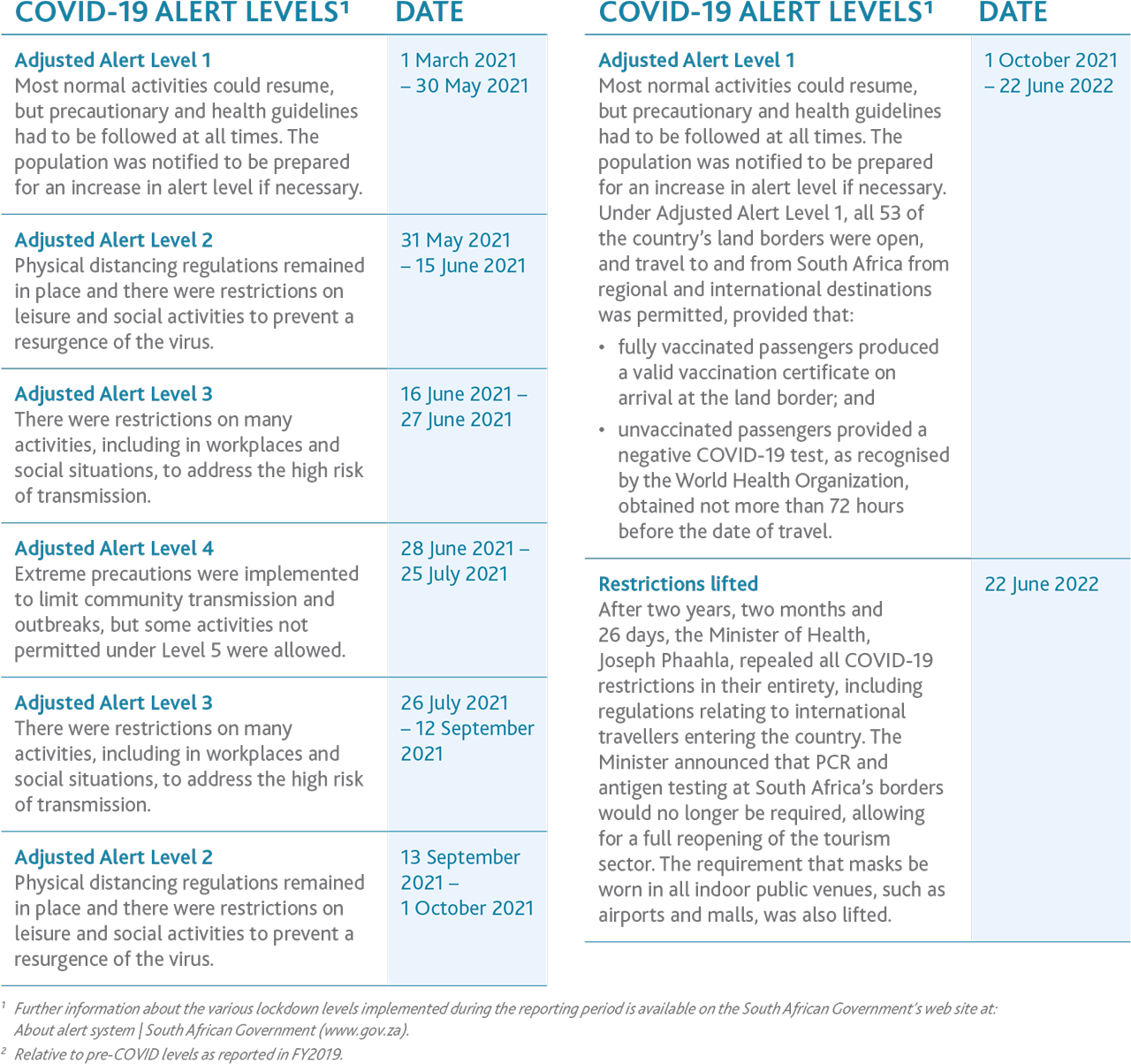

Throughout the reporting period, the ongoing COVID-19 pandemic continued to impact severely on our operations. In response to the various levels of lockdown and related travel restrictions, it remained necessary for us to restrict operations from time to time, which not only affected operational efficiency, but naturally also revenue. This was exacerbated by having to mothball some of our infrastructure, which made it difficult to respond to increases and decreases in passenger numbers as lockdown levels changed.

On a day-to-day basis, we were faced with the challenge of having to implement mandatory screening, social distancing and other measures in line with SACAA regulations. This meant that we had to rapidly acquire and deploy new screening technologies and additional staff, all of which pushed up operational expenditure at a time when revenue was under extreme pressure.

The Capital and Operational Expenditure Reduction Programme, which was introduced in the prior period, nevertheless enabled us to support our essential activities. Despite having to function under such constrained circumstances, we were therefore able to meet all of our operational obligations and maintain liquidity.

External factors that had a further impact on operations included the fact that a number of airlines had to be liquidated as a result of the pandemic, which had a knock-on effect on seating capacity, flight frequency and pricing, all of which, in turn, had a direct influence on operations, operational expenditure and revenue.

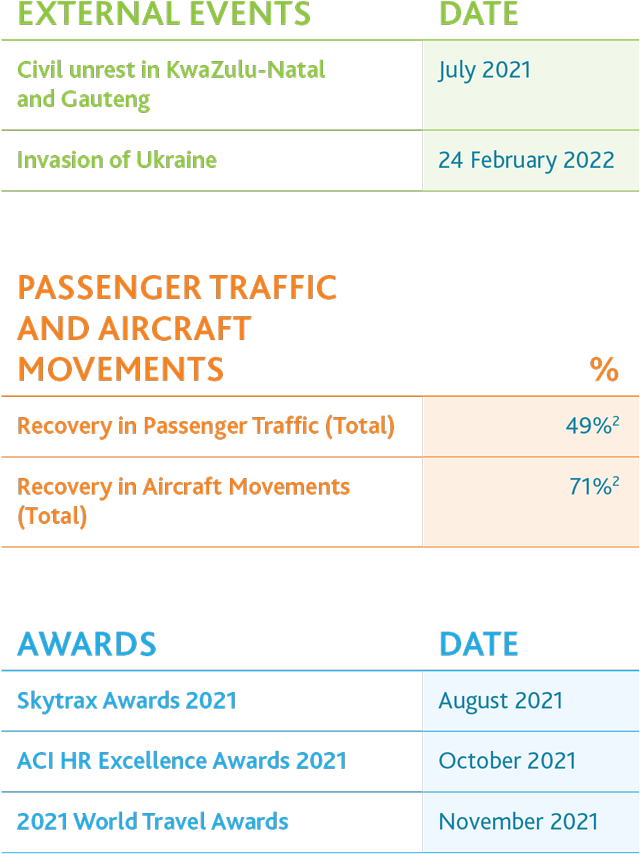

The civil unrest in Gauteng and KwaZulu-Natal in July 2021 came as an additional blow, disrupting not only passenger and cargo operations in the short term, but also having a notable impact on passenger confidence, which led to a decline in travel – especially from international destinations – for some time.

In February 2022, a further external shock came with the invasion of Ukraine, which had an almost immediate impact of the price of jet fuel and, in turn, on ticket prices.

There is a high level of uncertainty associated with this conflict and it is still too early to tell what the full extent of the repercussions will be. An internal risk analysis conducted by our GE of Strategy and Sustainability has indicated that, if the war becomes protracted, fundamentals shifts in the way in which energy is traded and supplied could cause a reconfiguration of the global geopolitical and economic order, with a number of different scenarios all being a possibility.

In the short term, the impact on aviation is already being felt and the knock-on effect on ticket prices, travel patterns and cargo volumes is a significant challenge we face in the current period (FY2023).

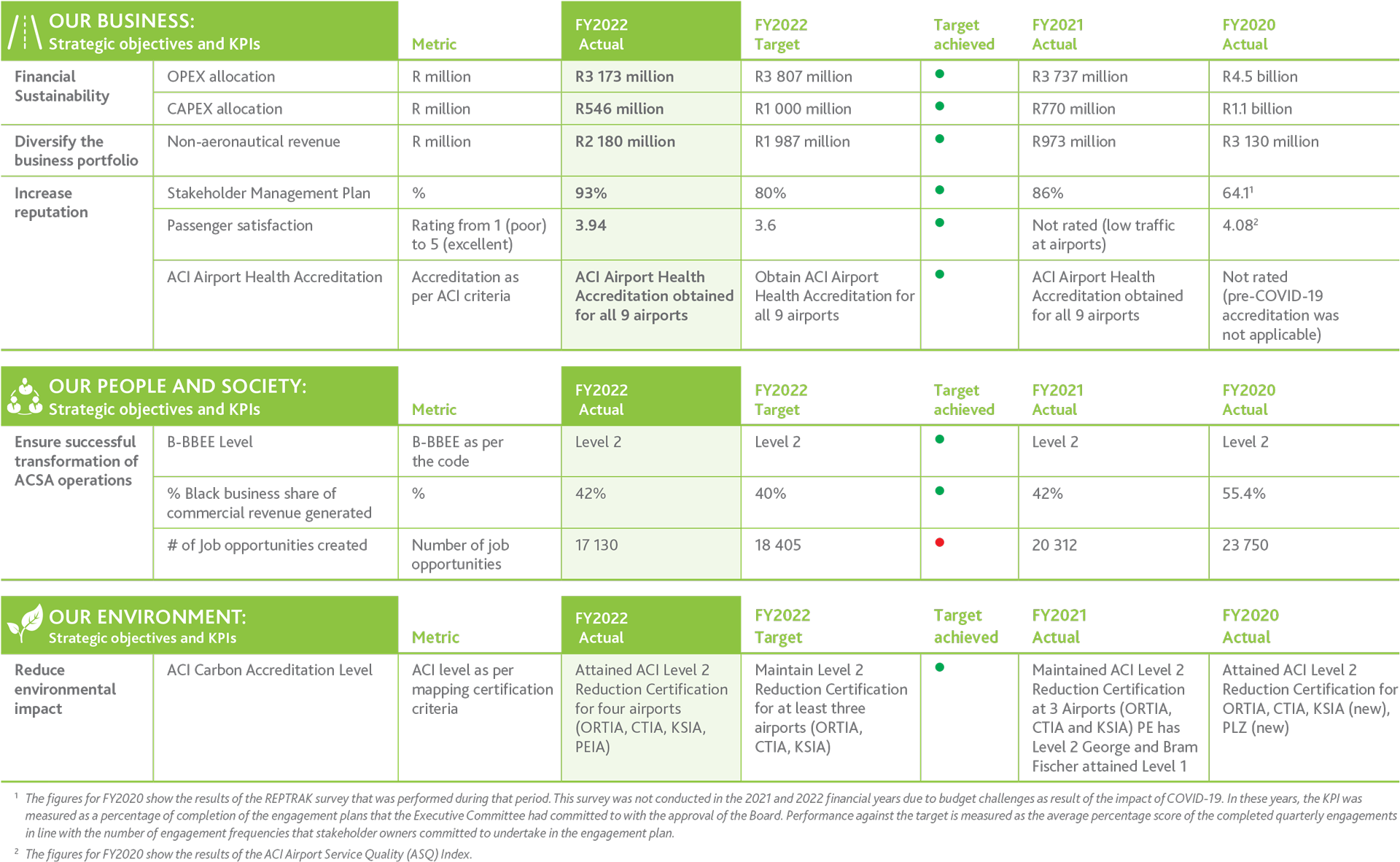

These challenges notwithstanding, all of our airports recorded an increase in passenger numbers during the reporting period and we are well positioned to support a recovery in both air travel and cargo volumes across all of our routes. Our performance report for the year gives detailed insight into our operational activities during the period.