As in the previous period, our operating environment continued to be defined by the ongoing COVID-19 pandemic and the mandatory measures that had to be implemented to contain the spread of the novel coronavirus.

At global level, supply chains continued to be constrained and the rand demonstrated a high level of volatility, especially towards the end of the reporting period. And as air travel all but ground to a halt in 2020 and the first half of 2021, we had to continue mothballing large sections of our infrastructure in order to contain costs.

While South Africa’s economy began to recover when lockdown restrictions started to be eased, the country’s annualised growth rate of 4.9% for 2021 did not fully offset the contraction of 6.4% in 2020, effectively placing it on a similar level to the third quarter of 2017 (Stats SA) by the end of the calendar year (Stats SA). This naturally had far-reaching socio-economic consequences, which were graphically demonstrated by the country recording its highest unemployment rate ever during the course of the year. And as analysts predict that growth in 2022 is likely to be much lower than it was in 2021, it is anticipated that the economy will take many years to recover to pre-COVID-19 levels.

Events like the civil unrest in KwaZulu-Natal and Gauteng in July 2021 and the return of Level 4 loadshedding in early 2022 only served to dampen consumer and investor confidence further, exacerbating the constraints on the aviation industry in general and on Airports Company South Africa in particular. Airlines had no other option but to cut flights and even routes, resulting in some local operators not being able to sustain their businesses.

A further shock came in the form of the war in Ukraine, which soon resulted in an increase in fuel prices, introducing yet another level of uncertainty into the aviation industry. Although passenger travel, particularly domestic travel, began to recover in the third quarter of the reporting period, passenger numbers remained markedly below pre-pandemic levels. Our network nevertheless recovered 49% of its pre-COVID-19 passenger throughput during the reporting period, largely due to the implementation of our Recover and Sustain Strategy and our revised Financial Plan.

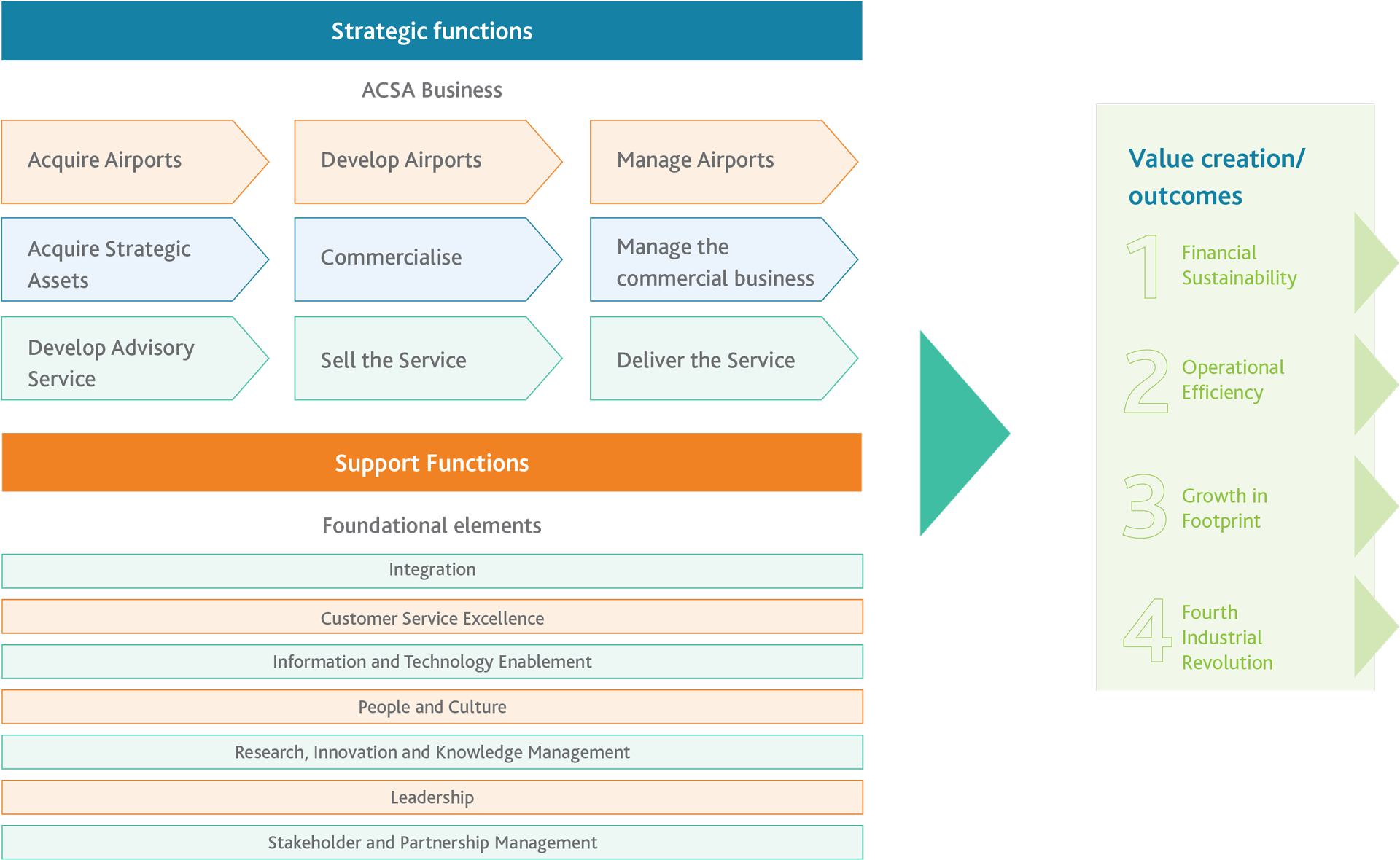

With ongoing uncertainty in travel and tourism, we are continuing to diversify our business into areas of non-aeronautical revenue to secure long-term sustainability. Our operating model has been adapted to reflect this and is given below.